Most organizations approach internal controls as compliance obligations rather than operational infrastructure. This creates a fundamental gap between documented procedures and actual risk management—a gap that becomes apparent when financial irregularities surface or audit findings reveal systemic weaknesses. The COSO audit framework addresses this disconnect by providing a structured methodology for designing, implementing, and evaluating internal controls that function as genuine risk mitigation mechanisms, not performative documentation.

For companies selling to enterprise clients, demonstrating robust internal control systems isn't merely advantageous—it's prerequisite. Enterprise procurement teams scrutinize vendors' governance structures, financial reporting reliability, and operational discipline before awarding contracts. The COSO frameworks are designed to help improve organizational performance in areas that include business operations, corporate reporting, regulatory compliance and risk management. Organizations implementing COSO principles signal to prospective enterprise buyers that their internal operations meet institutional standards for transparency, accountability, and risk management.

The framework's relevance extends beyond vendor qualification. COSO establishes a common language for discussing internal controls with auditors, investors, board members, and regulators. When stakeholders reference "effective internal controls," they're typically evaluating against COSO criteria—whether explicitly acknowledged or not. Understanding this framework allows organizations to align their control environments with the expectations of sophisticated enterprise clients who demand evidence of operational maturity.

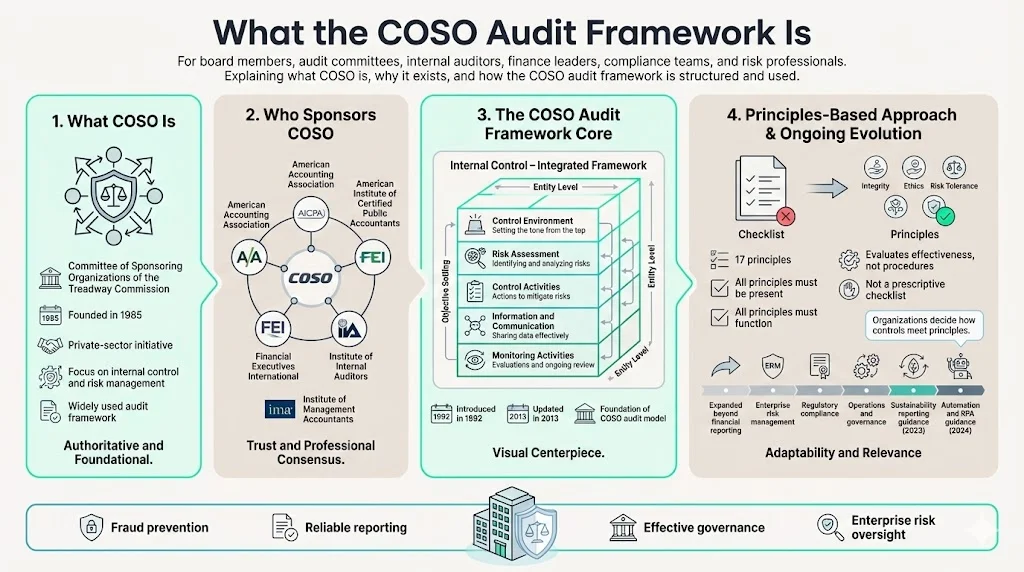

What the COSO Audit Framework Is

The COSO frameworks are documents that provide guidance on establishing internal controls and enterprise risk management (ERM) programs in organizations. Collectively, the frameworks are designed to help improve organizational performance in areas that include business operations, corporate reporting, regulatory compliance and risk management.

The Committee of Sponsoring Organizations of the Treadway Commission, which is commonly known as COSO developed the frameworks. Founded in 1985, COSO is a private sector body that's jointly sponsored by five professional associations: the American Accounting Association, the American Institute of Certified Public Accountants, Financial Executives International, the Institute of Internal Auditors, and Institute of Management Accountants.

COSO's original goal was to combat fraudulent financial reporting, but its scope has expanded. The organization now maintains multiple frameworks, with the Internal Control—Integrated Framework serving as the foundation for what's commonly referenced as the "COSO audit framework." The internal control framework, introduced by COSO in 1992 and updated in 2013, is detailed in a publication titled "Internal Control -- Integrated Framework."

The 2013 update represented a significant evolution, codifying 17 principles across the framework's five components and requiring organizations to demonstrate all principles are present and functioning for the overall system to be considered effective. This principles-based approach distinguishes COSO from prescriptive checklists—it establishes criteria for evaluating control effectiveness rather than mandating specific procedures. Organizations must determine how to satisfy each principle within their operational context, creating flexibility while maintaining rigorous standards.

COSO continues developing supplemental guidance addressing emerging risk areas. A publication with guidance on using the framework to help govern the use of robotic process automation technology was released in 2024, and one on implementing internal controls for sustainability reporting was issued in 2023. These updates ensure the framework remains relevant as business environments evolve.

Turning a risk framework into something auditors accept?

Drop your work email and we'll help you build a risk process that produces the evidence on its own.

Why Enterprise-Focused Businesses Should Care

Enterprise procurement processes evaluate vendor stability, operational maturity, and governance quality before establishing partnerships. Organizations lacking demonstrable internal control frameworks face immediate disadvantage—enterprise buyers interpret absent or immature controls as indicators of operational risk, financial unreliability, and potential business continuity vulnerabilities.

Strong internal controls directly correlate with stakeholder trust. Enterprise clients require confidence that vendors will deliver consistently, report financial performance accurately, protect sensitive data, and maintain operational continuity under adverse conditions. COSO implementation provides the structural foundation for these assurances. When vendors articulate their control environment using COSO terminology and demonstrate adherence to its principles, enterprise procurement teams recognize a credible governance infrastructure.

The framework's relevance extends across stakeholder categories. External auditors evaluate internal controls against COSO criteria when rendering opinions on financial statements. Investors assess control effectiveness when evaluating investment risk. Regulators reference COSO principles when examining compliance with financial reporting requirements. Board members rely on COSO-aligned controls when fulfilling their fiduciary oversight responsibilities. For organizations pursuing enterprise relationships, fluency in COSO principles facilitates communication across all these critical stakeholder groups.

Organizations demonstrating COSO alignment gain competitive advantages in enterprise sales cycles. When RFPs inquire about internal control frameworks, vendors citing COSO implementation with documented evidence of the five components and 17 principles operating effectively differentiate themselves from competitors offering generic assurances about "strong controls." This specificity signals operational maturity that enterprise buyers value—particularly in regulated industries or when vendor relationships involve access to sensitive data or critical business processes.

Core Concepts of the COSO Framework

Internal Controls in the COSO Context

COSO defines internal control as a process—not a static state or one-time implementation. This process-oriented definition recognizes that controls must adapt continuously to changing risks, evolving business models, and emerging threats. The framework positions internal control as a mechanism effected by an organization's board of directors, management, and personnel throughout the entity, emphasizing that control effectiveness depends on human judgment and execution, not merely documented procedures.

Internal controls within the COSO context serve three primary objectives: operations effectiveness and efficiency, financial reporting reliability, and compliance with applicable laws and regulations. Controls supporting operational objectives address resource utilization, asset protection, and strategic goal achievement. Financial reporting controls ensure information accuracy, completeness, and timeliness. Compliance controls maintain adherence to regulatory requirements and internal policies.

Critically, COSO acknowledges that internal controls provide reasonable—not absolute—assurance regarding objective achievement. This recognition addresses the reality that controls can fail due to human error, management override, or collusion. Organizations implementing COSO must calibrate control investments against risk tolerance, accepting that eliminating all risk is neither economically feasible nor operationally practical.

The Role of Risk Management

Risk assessment forms a core component of the COSO framework, positioning risk identification and analysis as prerequisites for effective control design. Organizations cannot implement appropriate controls without first understanding the specific risks threatening objective achievement. This risk-based approach prevents the common dysfunction of implementing generic controls disconnected from actual organizational risk profiles.

COSO's Enterprise Risk Management — Integrated Framework is the cornerstone of modern risk management practices. While the Internal Control—Integrated Framework addresses risk assessment as one component, COSO's separate ERM framework provides comprehensive guidance for organizations seeking to establish enterprise-wide risk management programs. The two frameworks complement each other—ERM establishes the broader risk management infrastructure, while internal controls provide specific mechanisms for managing identified risks.

The risk management component within COSO's internal control framework requires organizations to specify objectives with sufficient clarity to enable risk identification, identify risks to objective achievement, assess risk significance and likelihood, and determine appropriate risk responses. This systematic approach ensures control activities address actual risks rather than theoretical concerns, improving control effectiveness while reducing unnecessary control overhead.

Corporate Governance and Audit Standards

COSO aligns directly with corporate governance structures by establishing clear expectations for board oversight, management accountability, and operational discipline. The framework's control environment component explicitly addresses governance roles, requiring boards to maintain independence from management, exercise oversight responsibilities, and establish organizational structures with appropriate authority and responsibility assignments.

External auditors rely extensively on COSO when evaluating internal control effectiveness, particularly for financial reporting. Organizations subject to Sarbanes-Oxley Act requirements must demonstrate effective internal control over financial reporting—a determination auditors make by assessing COSO framework implementation. Even organizations not subject to SOX find that auditors evaluate control effectiveness using COSO criteria, making framework familiarity essential for productive audit relationships.

The framework supports regulatory compliance by providing structured methodologies for identifying applicable requirements, implementing controls to ensure compliance, and monitoring control effectiveness. Regulators examining organizational compliance frequently reference COSO principles when evaluating whether entities have established appropriate control infrastructures. This regulatory recognition makes COSO implementation valuable not merely for internal operational benefits but also for demonstrating compliance readiness to external oversight bodies.

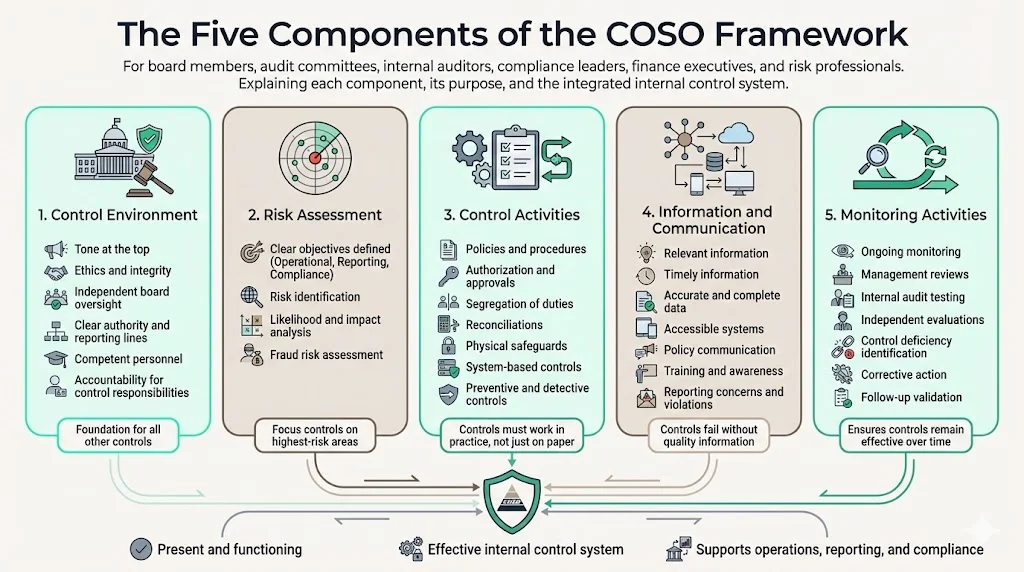

The Five Components of the COSO Framework

1) Control Environment

The control environment is a set of organizational standards, processes and structures that serve as the foundation for an internal control system. Without a strong control environment, individual control activities prove ineffective—employees circumvent procedures, management overrides controls, or ethical lapses undermine compliance efforts.

The control environment encompasses several critical elements. Tone at the top establishes leadership's commitment to integrity and ethical behavior, signaling throughout the organization that control circumvention is unacceptable. Board independence ensures governance oversight remains objective rather than deferential to management preferences. Organizational structure clarifies authority relationships and reporting lines, preventing control breakdowns due to ambiguous responsibilities. Human capital policies ensure the organization attracts, develops, and retains competent personnel aligned with control objectives.

Organizations building control environments must address five principles: demonstrating commitment to integrity and ethical values, exercising oversight responsibility through an independent board, establishing organizational structures with appropriate authority assignments, demonstrating commitment to competence by recruiting and developing qualified personnel, and holding individuals accountable for internal control responsibilities. These principles collectively create the cultural and structural foundation supporting all other framework components.

2) Risk Assessment

Risk assessment requires organizations to first establish clear objectives, then systematically identify and analyze risks that could prevent objective achievement. This component addresses both external risks (market changes, regulatory developments, technological disruption) and internal risks (process failures, personnel issues, system breakdowns).

Practical risk assessment in enterprise contexts begins with objective specification across operational, reporting, and compliance categories. Operational objectives might include achieving revenue targets, maintaining customer satisfaction levels, or delivering products within quality specifications. Reporting objectives ensure financial statements and management reports present accurate, complete information. Compliance objectives address adherence to laws, regulations, and internal policies.

Once objectives are specified, organizations identify risks through multiple mechanisms: management interviews, process walkthroughs, historical incident analysis, industry benchmarking, and emerging threat monitoring. Risk identification must address both the likelihood and potential impact of identified risks, enabling prioritization of control responses. Organizations facing numerous potential risks must focus control investments on those with highest likelihood or most severe impact, accepting residual risk in lower-priority areas.

COSO requires organizations to consider fraud risk specifically within risk assessment processes. This explicit fraud consideration recognizes that standard risk identification may overlook intentional misstatement, asset misappropriation, or corruption schemes. Organizations must assess fraud risks separately and implement specific controls addressing fraud prevention and detection.

3) Control Activities

Control activities are the policies, procedures, and practices organizations implement to address identified risks. These activities span multiple categories: authorization controls ensuring transactions receive appropriate approval, reconciliation controls detecting errors or irregularities, physical controls protecting assets, segregation of duties preventing single individuals from controlling all aspects of critical transactions, and information processing controls ensuring data accuracy and completeness.

Typical control activities in enterprise environments include approval hierarchies for expenditures, access controls limiting system permissions to authorized personnel, periodic reconciliations comparing recorded amounts to physical counts or external confirmations, management review of performance reports identifying anomalies, and automated controls embedded within information systems preventing or detecting policy violations.

Effective control activities share several characteristics. They address specific risks identified during risk assessment rather than generic concerns. They operate at appropriate frequency—some controls must function continuously, while others operate monthly, quarterly, or annually depending on risk profiles. They include both preventive controls (stopping errors before occurrence) and detective controls (identifying errors after occurrence). They're documented sufficiently that personnel understand requirements and auditors can evaluate effectiveness.

Organizations implementing control activities must avoid the common dysfunction of creating controls that appear robust in documentation but prove ineffective in practice. A purchase approval policy requiring three signatures means nothing if approvers routinely sign without reviewing supporting documentation. Control design must consider whether personnel have sufficient time, information, and authority to execute controls effectively.

4) Information and Communication

Internal controls cannot function without quality information flowing to appropriate personnel in sufficient time to enable control execution. The information and communication component addresses both information systems generating control-relevant data and communication channels distributing that information throughout the organization.

Quality information requirements include relevance (information addresses identified risks), timeliness (information reaches users when needed for decision-making or control execution), accuracy (data is correct and complete), and accessibility (authorized users can obtain required information efficiently). Organizations with poor information quality find that controls fail regardless of design sophistication—approvers lack data necessary for informed authorization decisions, reconcilers cannot access source documents for comparison, management reviews examine incomplete or inaccurate reports.

Communication requirements extend beyond information system outputs. Organizations must communicate control responsibilities to personnel, ensuring individuals understand their roles in the control environment. This includes communicating policies, procedures, and expectations; providing channels for reporting control deficiencies or suspected violations; and maintaining open communication with external parties including auditors, regulators, and business partners.

Enterprise organizations typically structure communication for controls through multiple mechanisms: policy manuals documenting control requirements, training programs educating personnel on control execution, performance evaluations incorporating control compliance assessments, and whistleblower hotlines enabling confidential reporting of suspected violations. These communication channels collectively ensure personnel throughout the organization understand control expectations and possess mechanisms for raising concerns.

5) Monitoring Activities

The framework aims to enable organizations to develop controls that can adapt to changing business environments, mitigate risks to acceptable levels and support effective decision-making and governance processes. Monitoring activities assess whether controls continue operating effectively over time, identifying deficiencies requiring remediation.

Monitoring includes both ongoing evaluations (routine supervisory activities, reconciliations, and management reports reviewed during normal operations) and separate evaluations (periodic assessments by internal audit teams or external consultants examining control effectiveness systematically). Most organizations employ both approaches—ongoing monitoring provides continuous control effectiveness indicators, while separate evaluations offer independent, objective assessment of overall control system health.

Internal audit teams play a critical role in monitoring activities, conducting periodic control testing across the organization and reporting findings to management and the board. Effective internal audit functions maintain independence from operations, possess sufficient technical competence to evaluate complex controls, and communicate findings transparently including identification of significant deficiencies requiring management attention.

Monitoring must include mechanisms for corrective action when deficiencies are identified. Organizations discovering control breakdowns must investigate root causes, implement remediation measures, and verify remediation effectiveness through follow-up testing. The monitoring component remains incomplete without this corrective action loop—identifying deficiencies without ensuring remediation leaves the organization exposed to the risks those controls were designed to address.

The COSO "Cube": Objectives Beyond Components

The COSO framework is frequently visualized as a three-dimensional cube representing the relationships between components, objectives, and organizational structure. This "COSO cube" illustrates that all five components must function across all three objective categories (operations, reporting, compliance) and at all organizational levels (entity-wide, division, operating unit, function).

The three objective categories address different organizational priorities. Operations objectives relate to effectiveness and efficiency of operations, including performance and profitability goals and safeguarding assets. Reporting objectives encompass both internal and external reporting, addressing financial and non-financial information reliability. Compliance objectives address adherence to laws and regulations applicable to the organization.

This multidimensional model emphasizes that internal control isn't monolithic—controls supporting financial reporting reliability may differ substantially from those ensuring regulatory compliance or operational effectiveness. Organizations must implement control components across all objective categories and organizational levels, recognizing that control requirements vary by context.

The cube visualization also illustrates that control assessment requires evaluation across multiple dimensions. An organization cannot claim effective internal controls by demonstrating a strong control environment without verifying that risk assessment, control activities, information and communication, and monitoring also function effectively across operations, reporting, and compliance objectives at all organizational levels. This comprehensive assessment requirement prevents organizations from claiming control effectiveness based on isolated strengths while overlooking systematic weaknesses.

Implementation Tips for Enterprise-Oriented Businesses

Organizations implementing COSO should begin with leadership commitment and education. Senior executives and board members must understand framework requirements and endorse implementation efforts. Without visible leadership support, personnel throughout the organization will treat COSO implementation as a compliance burden rather than an operational improvement initiative, undermining effectiveness.

Initial implementation steps include establishing a project team with representatives from finance, operations, compliance, internal audit, and information technology; documenting current control practices to identify gaps against COSO requirements; prioritizing implementation based on risk significance and resource availability; and developing implementation timelines with defined milestones and accountability assignments.

Documentation requirements deserve particular attention. Organizations must document their control environment, risk assessment processes, control activities, information and communication mechanisms, and monitoring procedures. This documentation serves multiple purposes: training new personnel, providing evidence for auditors, supporting management assessments of control effectiveness, and facilitating control improvements over time. Documentation should be sufficient that informed parties can understand what controls exist, how they operate, and who executes them.

Control testing establishes whether implemented controls operate effectively. Organizations should develop testing protocols examining control design (whether controls, if operating as prescribed, would effectively address identified risks) and operating effectiveness (whether controls actually operated throughout the testing period). Testing typically involves selecting samples of transactions and examining evidence that controls functioned—approval signatures exist, reconciliations were performed, exception reports were reviewed and resolved.

Integration with existing enterprise systems enhances implementation efficiency. Organizations already maintaining enterprise risk management programs, compliance management systems, or internal audit functions should leverage these existing capabilities rather than creating parallel structures. COSO implementation works most effectively when embedded within existing management processes rather than treated as separate initiatives requiring dedicated resources indefinitely.

Senior leadership buy-in proves critical throughout implementation, not merely at project initiation. Leaders must reinforce control importance through communications, resource allocation decisions, and personnel accountability systems. When leaders demonstrate that control effectiveness influences performance evaluations, promotion decisions, and compensation, personnel recognize that control compliance represents genuine organizational priority rather than bureaucratic formality.

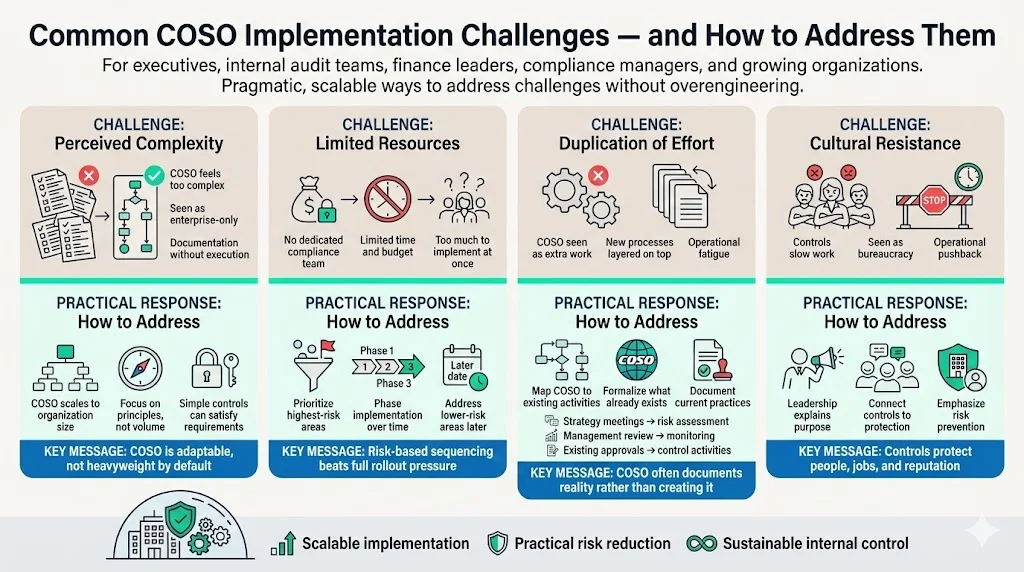

Common Challenges and How to Address Them

Organizations frequently perceive COSO as complex and resource-intensive, particularly smaller companies lacking dedicated compliance or internal audit functions. This perception leads to implementation avoidance or superficial adoption that documents controls without ensuring effective operation. The reality is that COSO principles scale across organizational sizes—small companies can implement simplified controls satisfying framework requirements without enterprise-scale infrastructure.

Smaller organizations should focus on foundational elements first. Establishing a strong control environment through leadership commitment to integrity, clear authority assignments, and accountability mechanisms provides control foundation without requiring extensive resources. Risk assessment can occur through management discussion sessions rather than formal risk registers and quantitative scoring methodologies. Control activities can leverage management review and supervision rather than automated system controls requiring significant technology investment.

Resource constraints present legitimate challenges, particularly for organizations attempting comprehensive implementation rapidly. Organizations should prioritize implementation based on risk significance, implementing controls addressing highest-risk areas first and addressing lower-priority risks over time as resources permit. This phased approach allows organizations to achieve meaningful risk reduction without overwhelming available resources.

Integration with existing processes addresses the common complaint that COSO creates additional work without corresponding operational benefits. Organizations should examine how COSO requirements align with activities already underway—risk identification discussions likely occur during strategic planning processes, control activities may already exist but lack formal documentation, monitoring activities may happen informally through management supervision. By formalizing and documenting existing practices rather than creating entirely new procedures, organizations can achieve COSO compliance without proportional workload increases.

Resistance from operational personnel who view controls as impediments to productivity requires cultural address through leadership communication and demonstration of control benefits. Leaders must articulate how controls protect the organization from risks that could jeopardize employment, damage reputation, or create liability. When personnel understand that controls serve protective functions rather than bureaucratic compliance, resistance typically diminishes.

Benefits of Using the COSO Audit Framework

Organizations implementing COSO experience improved assurance in internal controls and financial reporting reliability. By systematically addressing control design, implementation, and monitoring across all organizational areas, companies reduce the likelihood of financial misstatement, operational failures, or compliance violations. This improved reliability enhances stakeholder confidence—investors, lenders, and business partners gain assurance that the organization manages its affairs responsibly.

Risk visibility and preparedness improve substantially under COSO implementation. The framework's risk assessment component forces organizations to systematically identify and analyze risks that might otherwise remain unrecognized until materializing. This proactive risk identification enables preventive action rather than reactive crisis management, reducing both risk likelihood and impact when risks do materialize.

Governance benefits extend beyond compliance. COSO implementation clarifies roles and responsibilities throughout the organization, improves board oversight capabilities through enhanced reporting and monitoring, and establishes accountability mechanisms ensuring personnel take control responsibilities seriously. These governance improvements create organizational discipline that enhances performance beyond narrow compliance objectives.

Enterprise-level trust represents perhaps the most significant benefit for organizations pursuing large client relationships. Enterprise buyers consistently indicate that vendor governance, financial stability, and operational maturity influence purchasing decisions—particularly for strategic partnerships involving long-term commitments or access to sensitive data. Organizations demonstrating COSO alignment signal to enterprise prospects that their internal operations meet institutional governance standards, differentiating themselves from competitors lacking demonstrable control frameworks.

Conclusion

The COSO audit framework provides structured methodology for designing, implementing, and evaluating internal controls that function as genuine risk mitigation mechanisms rather than compliance theater. For organizations pursuing enterprise clients, framework implementation moves beyond regulatory compliance to become competitive necessity—enterprise procurement processes evaluate vendor governance maturity, and COSO alignment provides credible evidence of operational discipline.

The framework's five components—control environment, risk assessment, control activities, information and communication, and monitoring—establish comprehensive requirements spanning organizational culture, systematic risk analysis, specific control procedures, information infrastructure, and ongoing effectiveness assessment. Organizations must implement all components across operations, reporting, and compliance objectives at all organizational levels to claim effective internal controls.

Implementation requires leadership commitment, systematic planning, adequate documentation, control testing, and integration with existing management processes. While resource constraints and perceived complexity present legitimate challenges, organizations can scale COSO principles to their size and sophistication, achieving meaningful risk reduction without enterprise-scale infrastructure.

Structured internal controls matter for businesses targeting large clients because enterprise buyers demand governance assurance before establishing strategic partnerships. Organizations demonstrating COSO implementation through documented evidence of framework components operating effectively differentiate themselves in competitive enterprise sales cycles, signaling operational maturity that risk-conscious enterprise procurement teams value. In markets where trust and reliability determine vendor selection, COSO implementation provides the foundation for the governance credibility enterprise relationships require.

FAQs

Q1: What is the COSO audit framework?

The COSO audit framework refers to the Internal Control—Integrated Framework developed by the Committee of Sponsoring Organizations of the Treadway Commission. It provides structured guidance for designing, implementing, and evaluating internal controls supporting operational effectiveness, financial reporting reliability, and regulatory compliance. The framework comprises five components (control environment, risk assessment, control activities, information and communication, monitoring) and 17 principles organizations must demonstrate are present and functioning for effective internal control.

Q2: How does the COSO framework support internal controls and risk management?

COSO positions risk assessment as a prerequisite for effective internal control design. Organizations must first identify and analyze risks threatening objective achievement, then implement control activities specifically addressing those risks. The framework requires ongoing monitoring to ensure controls continue operating effectively as risks evolve. This risk-based approach ensures control investments address actual organizational risk profiles rather than generic concerns, improving both control effectiveness and resource efficiency.

Q3: What are the five components of the COSO framework?

The five components are: (1) Control Environment—organizational culture and governance structures establishing the foundation for internal control; (2) Risk Assessment—systematic identification and analysis of risks to objective achievement; (3) Control Activities—policies and procedures implemented to address identified risks; (4) Information and Communication—quality information flows and communication channels supporting control execution; (5) Monitoring Activities—ongoing and separate evaluations assessing whether controls operate effectively over time, with corrective action mechanisms addressing identified deficiencies.

Q4: How does COSO relate to corporate governance?

COSO directly supports corporate governance by establishing expectations for board oversight, management accountability, and organizational discipline. The control environment component requires boards to maintain independence from management and exercise oversight responsibilities. The framework clarifies authority relationships and reporting lines throughout organizations. Risk assessment and monitoring components provide boards with systematic information about organizational risk exposure and control effectiveness, enabling informed governance decisions. External auditors evaluate internal controls using COSO criteria when rendering opinions on financial statements, making framework implementation essential for organizations demonstrating governance credibility to stakeholders.

Q5: Can small businesses use the COSO framework?

COSO principles scale across organizational sizes. Small businesses can implement simplified controls satisfying framework requirements without enterprise-scale infrastructure. Smaller organizations should focus on foundational control environment elements through leadership commitment to integrity, clear authority assignments, and accountability mechanisms. Risk assessment can occur through management discussions rather than formal quantitative methodologies. Control activities can leverage management review and supervision rather than automated system controls requiring significant technology investment. The framework's principles-based approach provides flexibility for organizations to determine appropriate implementation methods within their resource constraints and risk profiles.