Most organizations evaluating emerging technologies focus on feature sets and deployment timelines. This approach overlooks a fundamental risk factor: whether the solution provider has survived the Valley of Death—the critical transition phase where promising innovations fail to achieve commercial viability. Understanding this concept enables enterprises to assess vendor stability, technology maturity, and partnership risk with greater precision.

The Valley of Death describes the gap between initial research outputs and commercially sustainable products. For enterprise buyers, this period signals heightened vendor risk: inadequate funding, unvalidated business models, and technology that appears functional in controlled environments but lacks the robustness required for production deployments. Companies that cannot identify where potential partners sit within this gap expose themselves to failed implementations, stranded investments, and operational disruption.

Three dynamics define this phase: funding misalignment between public research support and private capital requirements, technology readiness gaps where prototypes cannot scale to enterprise demands, and commercialization barriers where technical teams lack market expertise. Organizations evaluating startups, emerging security tools, or novel compliance technologies must assess these factors before committing resources.

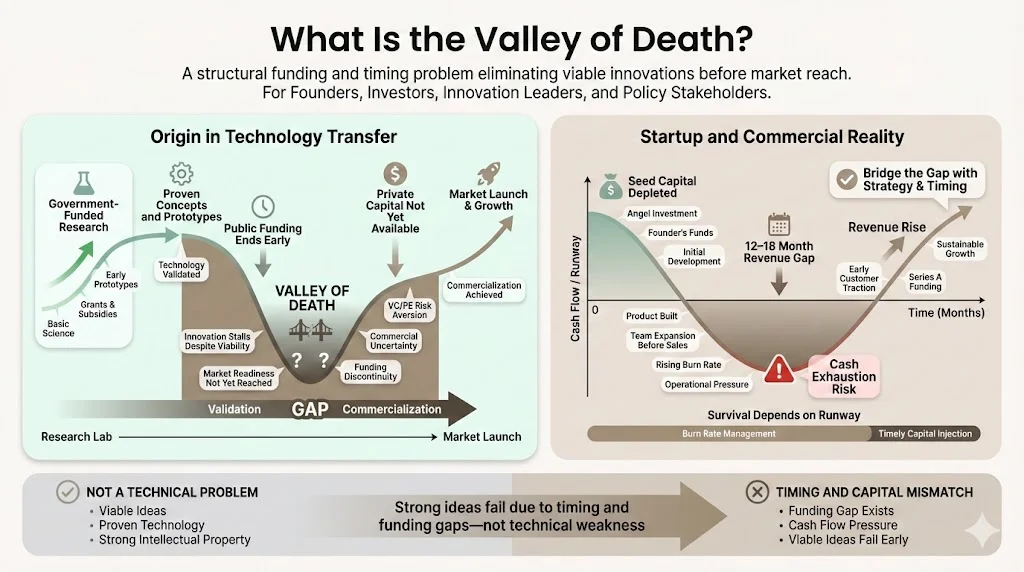

What Is the Valley of Death?

The term originated in technology transfer literature to describe the transition gap between laboratory research and commercial manufacturing. Government-funded research produces validated concepts and prototypes, but public funding typically terminates before products reach market readiness. Private investors, conversely, require demonstrated market traction and revenue before committing capital. This creates a funding void where technically sound innovations collapse due to resource depletion rather than technical failure.

In startup contexts, the Valley of Death represents the operational period between product development and sustainable revenue generation. Companies in this phase have exhausted seed capital, face 12-18 months before meaningful customer contracts materialize, and lack sufficient cash reserves to bridge the gap. Burn rates accelerate as teams expand for commercial launch while revenue remains minimal—a structural mismatch that eliminates otherwise viable businesses.

Key Characteristics

Innovation gap: The distance between a working prototype demonstrated under controlled conditions and a product capable of operating reliably within complex enterprise environments. This gap encompasses scalability requirements, integration complexity, security hardening, and support infrastructure that early-stage companies systematically underestimate.

Funding shortage: Public research grants terminate at Technology Readiness Level (TRL) 4-5, while venture capital typically enters at TRL 7-8 once commercial validation exists. The intermediate stages—critical for transitioning from concept to product—receive inadequate financial support from either source.

Technological risk: Early-stage technologies exhibit functional capabilities under specific conditions but lack the resilience, error handling, edge case management, and interoperability required for enterprise deployment. Security controls may satisfy proof-of-concept requirements while failing audit scrutiny when implemented at scale.

Commercialization barriers: Technical founders frequently lack expertise in contract negotiation, enterprise sales cycles, regulatory compliance navigation, and customer success operations. This skills gap transforms technically superior solutions into commercial failures when teams cannot translate capabilities into value propositions that procurement departments recognize.

Where It Shows Up in Practice

Pre-Series A and early Series B funding stages represent peak Valley of Death exposure. Companies have developed functional products and secured initial customers but lack sufficient runway to achieve profitability or demonstrate the metrics required for subsequent funding rounds. Burn rates of $150,000-$300,000 monthly create 9-12 month survival windows that cannot accommodate the 14-18 month enterprise sales cycles they face.

Research institutions and university technology transfer offices consistently encounter this gap when commercializing inventions. Discoveries validated through peer review and prototype testing cannot attract licensing partners or spinout investment because they sit at TRL 4-6—too early for commercial partners, too late for additional research funding.

Corporate innovation pipelines experience internal versions of this phenomenon when pilot projects demonstrate technical feasibility but cannot secure operational budgets for full deployment. Internal teams struggle to justify investment in unproven solutions when competing against established vendors with documented performance records.

Building toward SOC 2, ISO 27001, or another framework?

Drop your work email and we'll help you turn security work into audit-ready evidence automatically.

The Purpose Behind the Concept

Making Innovation Manageable

The Valley of Death framework explains why technical excellence alone does not predict commercial success. Analysis of this gap reveals that most innovation failures stem from capital structure problems and commercialization process gaps rather than technological inadequacy. This distinction matters for enterprises: dismissing failed vendors as "poor technology choices" when structural factors caused collapse leads to repeatedly selecting partners facing identical risks.

Documenting this phenomenon enables stakeholders to implement targeted interventions rather than generic "innovation support" that fails to address specific bottlenecks. Enterprises can structure pilot programs that provide commercialization assistance alongside technical evaluation. Investors can design funding vehicles specifically for mid-TRL stages. Policymakers can target grants at the 12-18 month commercialization window where market gaps are most acute.

Bridging the Gap

Organizations that understand Valley of Death dynamics reduce risk exposure, accelerate technology adoption timelines, and improve capital allocation efficiency. Enterprises avoid premature commitments to vendors unlikely to survive their own sales cycles. They structure partnerships that share commercialization burdens rather than expecting startups to independently navigate enterprise procurement requirements.

Investors who recognize this gap deploy capital at stages where modest funding produces disproportionate impact—enabling companies to reach the revenue milestones that unlock subsequent funding rounds. This strategic positioning generates superior returns compared to late-stage investments where competition drives valuation multiples beyond risk-adjusted values.

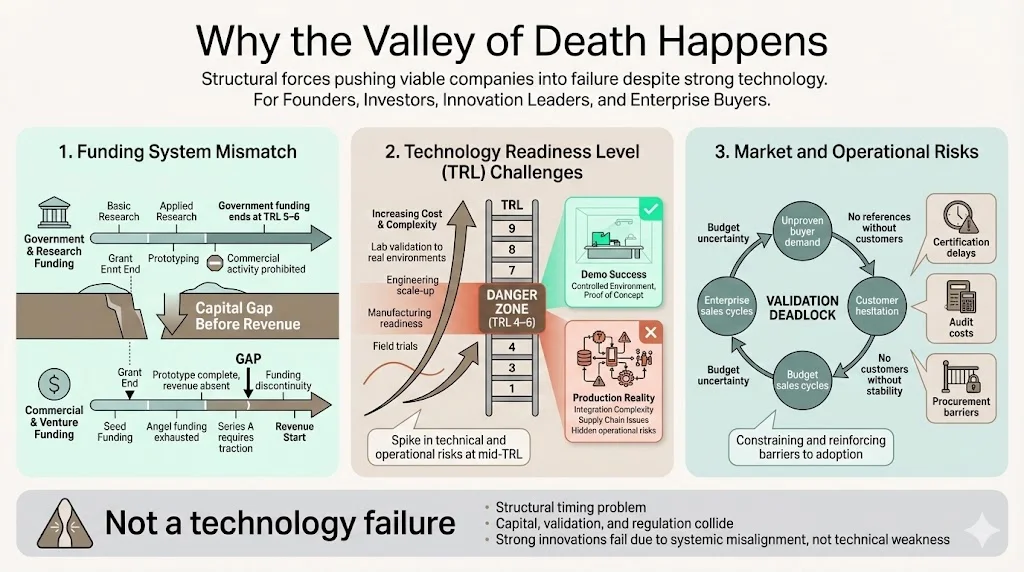

Why the Valley of Death Happens

1) Funding System Mismatch

Government research programs—including SBIR grants, DOE innovation initiatives, and NSF funding—support early discovery through TRL 5-6. These programs explicitly prohibit funding commercial activities, creating sharp termination points precisely when commercialization expenses accelerate. A company receiving a $1.5 million Phase II SBIR grant for prototype development faces immediate funding gaps when that research concludes but 18 months remain before customer contracts generate sufficient revenue.

Private investors assess opportunities through risk-adjusted return frameworks that favor later-stage deployments. Angel investors provide $500,000-$2 million for initial product development, but subsequent Series A rounds of $5-15 million require demonstrated product-market fit: recurring revenue, validated customer acquisition costs, and retention metrics. Companies requiring 24 months to develop these metrics after exhausting angel funding enter the Valley of Death—too advanced for seed investment, insufficiently proven for institutional capital.

2) Technology Readiness Level (TRL) Challenges

The TRL scale defines nine stages from basic research (TRL 1) through proven operational deployment (TRL 9). TRL 4-6 represents the most resource-intensive transition: moving from laboratory validation to prototype systems demonstrated in relevant environments. This phase requires expanding engineering teams, developing manufacturing processes, conducting field trials, and addressing integration challenges that controlled testing environments obscure.

Enterprise buyers evaluating security or compliance tools must assess vendor TRL positioning. A vulnerability management platform at TRL 5—validated in isolated test networks—differs fundamentally from TRL 8 solutions operating across diverse production environments. Purchasing decisions based on demo performance without TRL assessment create implementation risks: products that appeared functional in sales presentations fail when deployed against real infrastructure complexity, legacy system interactions, and operational constraints.

3) Market and Operational Risks

Technical teams building innovative solutions frequently lack business model validation. They understand the problem they are solving but have not confirmed that target customers recognize the problem severity, prioritize its resolution, or possess budgets allocated to solutions. This validation gap means companies build products for markets that do not materially exist—not because the technology fails, but because the value proposition does not align with how enterprises actually purchase and deploy solutions.

Customer validation requires enterprise buyers willing to participate in pilots, provide feedback, and serve as references—yet enterprises hesitate to engage vendors exhibiting Valley of Death characteristics. This creates circular dependency: startups need customer validation to attract funding and survive, but potential customers avoid engagement until companies demonstrate stability and resources to support deployments.

Regulatory requirements compound these challenges for security and compliance technologies. A startup developing novel authentication mechanisms faces certification requirements (FedRAMP, Common Criteria, SOC 2 Type II) that require 8-14 months and $150,000-$500,000 in audit costs before enterprise procurement departments permit evaluation. Companies entering the Valley of Death lack resources to complete these certifications, eliminating their addressable market precisely when revenue becomes critical.

Why It Matters to Enterprise Buyers

1) Evaluating Emerging Technologies

Enterprises assessing emerging security tools, compliance platforms, or infrastructure innovations must determine whether vendors possess sufficient resources to complete implementations, provide ongoing support, and maintain product development roadmaps. A vendor 8 months from capital depletion presents unacceptable risk regardless of technical superiority—failed vendors create stranded investments, implementation restarts, and operational disruptions that exceed any performance advantages their solutions offer.

Due diligence processes should explicitly assess vendor funding runway, burn rate relative to revenue growth, and proximity to subsequent funding milestones. Companies with 6-month runways and no clear path to Series B financing sit in the Valley of Death's most dangerous phase. Enterprises engaging such vendors must structure agreements acknowledging this risk: limited initial commitments, milestone-based expansion, and contingency plans for vendor failure.

2) Strategic Partnerships and Risk Sharing

Co-development arrangements enable enterprises to access innovative technologies while mitigating Valley of Death risks. Rather than waiting for startups to independently achieve commercial readiness, strategic partnerships provide capital, market access, and operational expertise in exchange for early adoption rights or equity participation. This approach benefits both parties: enterprises gain competitive advantage through early access to differentiated capabilities; startups secure resources to traverse commercialization gaps.

Corporate venture arms structured to invest in mid-TRL companies bridge funding gaps that traditional VC models cannot address. A $2-3 million strategic investment from an enterprise buyer provides startups with 12-18 month runway extensions while giving the enterprise partner influence over product roadmaps, priority support access, and favorable commercial terms. These investments generate returns through operational benefits rather than purely financial multiples.

Pilot projects with clear success metrics and structured graduation paths help both parties manage risk. Rather than binary purchase decisions, enterprises can fund limited deployments that validate technology readiness while providing startups with reference customers and revenue that enable survival. Pilots structured with explicit commercialization milestones—demonstrated scalability to X users, integration with Y systems, achievement of Z performance benchmarks—create objective decision frameworks that reduce mutual risk.

3) Competitive Advantage

Organizations that can identify and support strong innovations before competitors gain first-mover advantages in rapidly evolving domains like zero-trust architecture, supply chain security, or AI governance. Companies waiting for technologies to achieve full market maturity face crowded vendor landscapes, premium pricing, and limited differentiation opportunities. Strategic engagement during Valley of Death phases enables enterprises to shape product development, secure preferential commercial relationships, and deploy capabilities before competitors recognize their significance.

This calculus requires balancing innovation benefits against execution risks. Enterprises with mature risk management capabilities, technical expertise to support immature technologies, and tolerance for vendor uncertainty can extract substantial value from early partnerships. Organizations lacking these capabilities should limit Valley of Death exposure—waiting for technologies to achieve commercial stability before commitment.

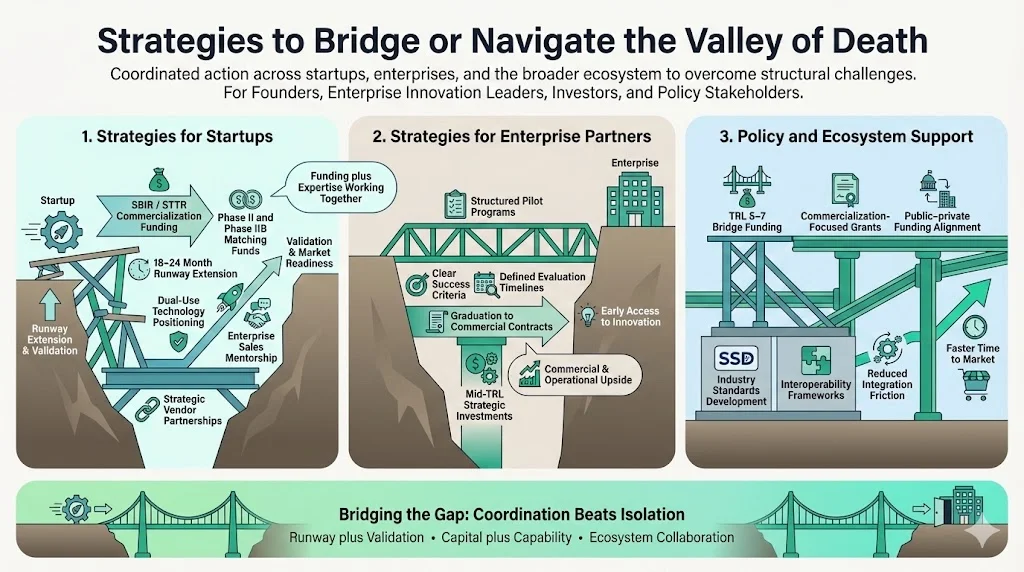

Strategies to Bridge or Navigate It

For Startups

SBIR/STTR programs provide non-dilutive funding specifically designed to support commercialization phases. Phase II grants of $1-2 million combined with Phase IIB matching funds from private partners can extend the runway by 18-24 months—sufficient to achieve the revenue milestones that attract Series A investment. Companies developing dual-use technologies applicable to government and commercial markets should pursue these programs systematically rather than viewing them as backup funding sources.

Accelerator programs offering not just capital but commercialization expertise address skills gaps that technical founders face. Programs like Techstars, Y Combinator, or industry-specific accelerators provide mentorship in enterprise sales, contract negotiation, and go-to-market strategy while connecting startups with potential customers and investors. The operational guidance these programs provide often matters more than their capital contributions for companies navigating Valley of Death challenges.

Strategic partnerships with established vendors create distribution channels and market validation that resource-constrained startups cannot build independently. A startup providing specialized security capabilities might partner with established SIEM vendors, gaining access to existing customer bases while the larger partner enhances their solution portfolio. These arrangements require careful negotiation to avoid unfavorable dependencies, but properly structured relationships enable Valley of Death navigation that would otherwise be impossible.

For Enterprise Partners

Structured pilots with explicit success criteria, defined evaluation periods, and clear graduation paths reduce risk for both parties. Rather than open-ended "innovation experiments," these arrangements specify technical requirements, performance benchmarks, and commercial terms that activate upon successful completion. This structure provides startups with predictable revenue opportunities while giving enterprises objective decision frameworks independent of vendor survival concerns.

Investment vehicles tailored to mid-TRL stages enable enterprises to support promising technologies through Valley of Death periods while maintaining strategic optionality. Rather than binary purchase decisions, enterprises can deploy $500,000-$2 million strategic investments that extend vendor runways while securing favorable commercial terms, early access to capabilities, and potential equity appreciation. These investments require different approval processes than traditional procurement but generate compounding returns through operational advantages and financial participation.

Expertise sharing arrangements where enterprises provide commercialization support—regulatory guidance, customer introductions, operational best practices—reduce startup resource requirements while building stronger partnerships. An enterprise CISO introducing a security startup to peer organizations provides market validation worth more than equivalent capital investments. Procurement teams that guide startups through enterprise sales processes accelerate commercialization while shaping solutions to fit actual enterprise requirements.

Policy and Ecosystem Efforts

Government grant programs specifically targeting TRL 5-7 technologies address the funding gap between research grants and commercial investment. The DOE's Technology Commercialization Fund, NIH's Bridge Awards, and similar initiatives provide $500,000-$3 million to support commercialization activities that neither research grants nor private investors fund adequately.

Industry-wide standardization efforts reduce technical risk by establishing common frameworks for interoperability, security requirements, and performance benchmarks. When vendors can develop to published standards rather than custom enterprise requirements, they reduce development costs and accelerate time-to-market—shortening Valley of Death exposure periods.

Examples and Case Points

Battery technology development illustrates classic Valley of Death dynamics. Researchers at national laboratories developed advanced lithium-ion chemistries with superior energy density and safety characteristics. These innovations achieved TRL 5-6 validation but required $50-100 million to establish manufacturing capabilities and complete automotive industry certifications. The gap between research funding termination and the scale required to attract manufacturing partners stranded multiple promising battery technologies. Successful cases like A123 Systems navigated this gap through DOE loan guarantees and strategic automotive partnerships—though even A123 faced near-failure before acquisition by Chinese interests. Companies that could not secure similar bridging resources saw their technologies abandoned despite technical superiority.

Cybersecurity mesh architectures emerged from research institutions and startup development throughout 2019-2022. Multiple companies developed functional prototypes demonstrating how distributed security controls could replace perimeter-based models. Most failed to achieve commercial viability despite technical validation—enterprises were not prepared to replace established architectures, integration complexity exceeded early-stage companies' implementation capabilities, and the 18-24 month sales cycles required resources these vendors lacked. The few successful commercializations occurred when established security vendors acquired promising technologies and integrated them into existing product portfolios, providing the resources and market access that standalone companies could not generate independently.

Government contracting contexts demonstrate particularly acute Valley of Death challenges. Defense Innovation Unit and AFWERX programs identify promising dual-use technologies and fund initial prototypes through SBIR-style contracts. However, progression from successful prototype to production contracts requires surviving the 18-36 month transition while federal procurement processes complete. Companies that cannot bridge this gap through commercial revenue or private investment collapse despite delivering successful prototypes—explaining why defense technology transitions show high technical success rates but low commercialization rates.

Conclusion

The Valley of Death represents a structural risk factor in innovation ecosystems where funding mechanisms, technology maturity requirements, and commercialization capabilities fail to align. For enterprises evaluating emerging technologies—particularly in security and compliance domains where vendor stability directly impacts operational risk—understanding where potential partners sit relative to this gap enables more accurate risk assessment and strategic partnership structuring.

Organizations that recognize Valley of Death dynamics can engage innovative vendors earlier and more safely through structured pilots, strategic investments, and expertise sharing that address commercialization gaps. This approach generates competitive advantages through early access to differentiated capabilities while supporting ecosystem health by enabling promising innovations to reach commercial viability. Conversely, enterprises that ignore these dynamics face repeated vendor failures, stranded investments, and missed opportunities to shape emerging technologies during their formative periods.

The concept remains critically relevant as emerging domains like AI governance, quantum-resistant cryptography, and zero-trust architectures follow familiar innovation patterns: promising research outputs, functional prototypes, and a commercialization gap that will eliminate most contenders before technologies achieve market maturity. Enterprise technology strategies must incorporate Valley of Death assessment as a standard due diligence component—not to avoid all early-stage risk, but to engage it strategically where potential returns justify calculated exposure.

FAQ Section

1) What is the Valley of Death in government contracting?

Government R&D programs fund technology development through prototype demonstration but typically terminate before commercial production capabilities exist. Defense and federal agencies often see successful research outcomes that cannot attract private sector manufacturing partners because technologies sit at TRL 5-7—too advanced for additional research funding, insufficiently mature for commercial investment. This gap explains why agencies report high prototype success rates but low transition rates to fielded capabilities. Companies developing government-funded innovations must independently bridge 18-36 months between prototype delivery and production contracts, a period most cannot survive without commercial revenue streams.

2) Why do startups fail in the Valley of Death?

Three factors drive Valley of Death failures: capital depletion before achieving sustainable revenue, market validation gaps where assumed demand does not materialize at predicted rates, and commercialization inexperience where technical teams lack enterprise sales capabilities. Startups systematically underestimate the resources and duration required to transform prototype demonstrations into production deployments. A security tool validated in controlled testing environments may require 12-18 additional months for enterprise integration, certification completion, and customer success infrastructure development—periods that consume $2-4 million beyond initial product development budgets. Companies entering this phase with insufficient reserves collapse regardless of technical merit.

3) How does TRL relate to the Valley of Death?

TRL 4-7 represents the Valley of Death's core range. TRL 4 indicates laboratory validation of integrated systems; TRL 7 signifies operational prototypes demonstrated in relevant environments. This transition requires expanding from controlled testing to field deployments, addressing integration challenges, completing regulatory certifications, and developing manufacturing processes. Research funding typically terminates at TRL 5-6, while private investors prefer TRL 7-8 where commercial viability is demonstrated. Technologies at TRL 5-6 sit precisely in the funding gap, requiring $2-10 million and 18-36 months to reach commercial readiness—resources that neither funding source adequately provides.

4) Can enterprise partnerships reduce the Valley of Death risk?

Strategic enterprise cooperation substantially mitigates Valley of Death risk through three mechanisms: providing revenue that extends startup runway, offering market validation that attracts subsequent investment, and contributing operational expertise that addresses commercialization gaps. Pilot contracts structured with clear graduation to production deployments give startups predictable revenue opportunities while enterprises evaluate technologies with limited commitment. Corporate venture investments of $1-3 million bridge funding gaps that traditional VC models do not address. Most importantly, enterprise partners provide customer references, regulatory guidance, and market access that resource-constrained startups cannot generate independently—reducing the time and capital required to achieve commercial sustainability.