Most organizations seeking enterprise customers encounter a common inflection point: procurement teams demand evidence of data protection controls before signing contracts. This requirement invariably surfaces questions about SOC reports, attestation standards, and the organization behind them—the American Institute of Certified Public Accountants. Understanding what the AICPA is and how its frameworks support data protection has become essential for vendors targeting enterprise buyers who require documented assurance that their service providers meet defined security and privacy criteria.

What is AICPA?

The American Institute of Certified Public Accountants (AICPA) is the national professional organization of Certified Public Accountants (CPAs) in the United States, with more than 428,000 members in 130 countries. Founded in 1887 as the American Association of Public Accountants (AAPA), the organization sets ethical standards and U.S. auditing standards. The AICPA established itself as the authoritative body responsible for CPA credentialing, professional conduct, and the development of auditing and attestation frameworks that underpin financial and operational assurance across industries.

Key functions and scope

The AICPA operates across multiple domains critical to the accounting profession and broader business ecosystem. It develops and grades the Uniform CPA Examination—the licensing exam required for all individuals seeking CPA certification. Beyond credentialing, the organization issues auditing standards, attestation standards, and maintains the AICPA Code of Professional Conduct, which establishes ethical requirements for CPAs and the firms employing them.

The AICPA's standard-setting authority extends to attest services, business valuation, tax practice, and CPA firm quality control. While the Financial Accounting Standards Board assumed responsibility for Generally Accepted Accounting Principles (GAAP) in the 1970s, the AICPA retained its leadership in auditing methodology, attestation frameworks, and professional ethics. This standard-setting function directly impacts how organizations demonstrate compliance, security posture, and data protection capabilities to enterprise clients and regulators.

The organization provides member services including continuing professional education, technical guidance, and advocacy before regulatory bodies. Members of the AICPA must attest annually to meeting the requirements for their membership types, complying with the AICPA's bylaws and upholding the AICPA's Code of Professional Conduct. This ongoing accountability ensures that CPAs conducting audits and attestations maintain competence and ethical standards.

Chasing a SOC 2 report to close enterprise deals?

Drop your work email and we'll map the controls and evidence you still need.

Why AICPA matters to enterprise-selling companies

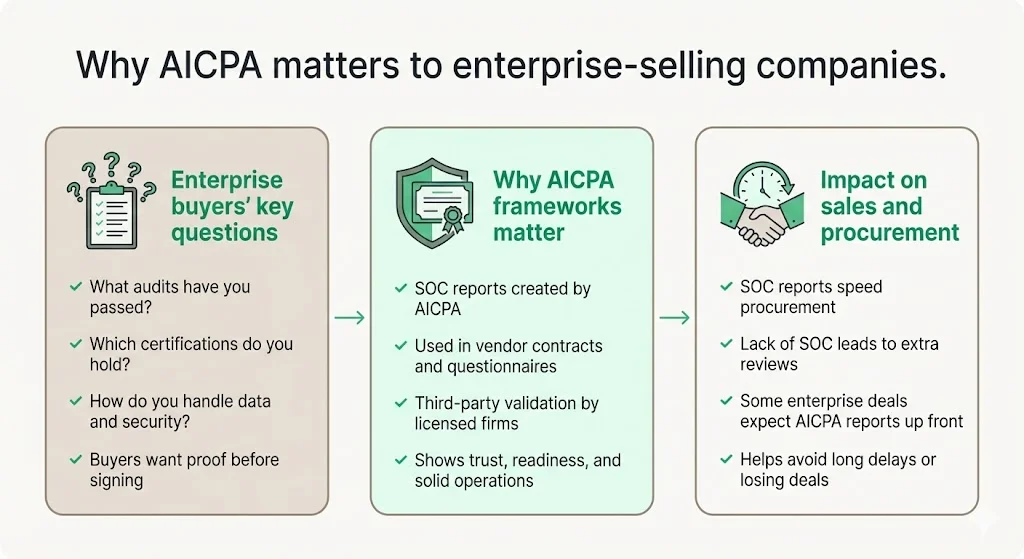

Enterprise buyers conducting vendor risk assessments consistently demand answers to three questions: What audits have you completed? What certifications do you hold? What assurances can you provide around data handling and security controls? These questions stem from enterprise risk management programs that require documented evidence of vendor security practices before contract execution.

AICPA-developed frameworks—particularly the System and Organization Controls (SOC) suite—have become the de facto standard referenced in vendor contracts, security questionnaires, and enterprise procurement processes. Organizations selling to enterprise clients benefit from aligning with these frameworks because they provide third-party validation conducted by licensed CPA firms following standardized criteria. This alignment signals trust, compliance readiness, and operational maturity in ways that internal security documentation cannot replicate.

For vendors targeting enterprise markets, demonstrating adherence to AICPA standards translates directly to contract velocity and competitive positioning. Procurement teams evaluate vendors based on attestation reports that follow AICPA-issued criteria, creating a threshold requirement for market entry rather than a differentiator. Organizations lacking SOC reports or equivalent AICPA-aligned attestations face extended procurement cycles, additional security reviews, and potential disqualification from enterprise opportunities.

How AICPA supports data protection standards

Overview of frameworks related to data protection

The AICPA developed the SOC suite—SOC 1, SOC 2, and SOC 3—specifically for service organizations that handle customer data or provide services affecting customer systems. SOC 2, the most widely adopted framework for data protection assurance, evaluates controls based on Trust Services Criteria (TSC). These criteria encompass five categories: security, availability, processing integrity, confidentiality, and privacy. Each category addresses specific control objectives related to how organizations protect data, maintain system availability, ensure accurate processing, safeguard confidential information, and handle personal data in compliance with privacy commitments.

Beyond SOC 2, the AICPA created SOC for Cybersecurity, a framework enabling organizations to report on enterprise-wide cybersecurity risk management programs. This framework addresses the growing demand from enterprise buyers for visibility into vendor cybersecurity governance, risk assessment processes, and incident response capabilities. The AICPA also developed Generally Accepted Privacy Principles (GAPP) in collaboration with the Canadian Institute of Chartered Accountants, establishing a framework for privacy program assessment and attestation.

Data-protection elements built into AICPA standards

Trust Services Criteria explicitly address confidentiality and privacy as distinct categories, requiring organizations to implement controls protecting sensitive data from unauthorized disclosure and ensuring personal information is collected, used, retained, and disclosed according to stated privacy commitments. The security criterion—applicable to all SOC 2 reports—establishes baseline requirements for access controls, logical and physical security, system operations, change management, and risk mitigation.

The AICPA Code of Professional Conduct imposes confidentiality obligations on CPAs conducting audits and attestations, creating accountability for how auditors handle client data during engagements. This ethical framework extends to the organization's CPAs audit; demonstrating compliance with Trust Services Criteria requires documented policies, procedures, and evidence showing that data-handling controls operate effectively over time.

SOC frameworks provide assurance through attestations issued by licensed CPA firms following standardized examination procedures. Unlike self-assessed certifications or vendor-generated security documentation, SOC reports require independent verification of control design and operating effectiveness. For SOC 2 Type II—the standard enterprise buyers typically require—auditors evaluate whether controls operated effectively over a minimum observation period, documenting exceptions and providing transparency into actual security operations rather than theoretical frameworks.

The cybersecurity and privacy frameworks add governance structures and reporting mechanisms that extend beyond traditional financial-control audits. These frameworks enable organizations to demonstrate board-level oversight, risk assessment methodologies, threat monitoring capabilities, and incident response readiness—elements increasingly scrutinized during enterprise vendor evaluations.

Why this matters for enterprise sellers

Enterprise clients increasingly require evidence of data protection practices to support contract risk assessments, vendor management programs, and regulatory compliance obligations. Organizations subject to regulations like GDPR, HIPAA, or sector-specific data protection requirements often cascade compliance expectations to vendors through contractual requirements for SOC 2 reports or equivalent attestations.

Aligning with AICPA frameworks enables vendors to embed data-protection assurance into procurement conversations. Rather than responding to security questionnaires with narrative explanations of internal practices, vendors can reference SOC 2 Type II reports demonstrating independent verification of controls aligned with Trust Services Criteria. This shifts the conversation from subjective claims to documented evidence validated by licensed auditors.

This positioning proves particularly valuable in competitive sales cycles where multiple vendors compete for enterprise contracts. Procurement teams often use SOC 2 status as an initial screening criterion, eliminating vendors without current attestations before detailed evaluations begin. Organizations maintaining audit readiness and current SOC reports reduce procurement friction and demonstrate operational discipline that extends beyond security to encompass process maturity and governance.

Implementation considerations for companies

What companies need to know when preparing for AICPA-related audits

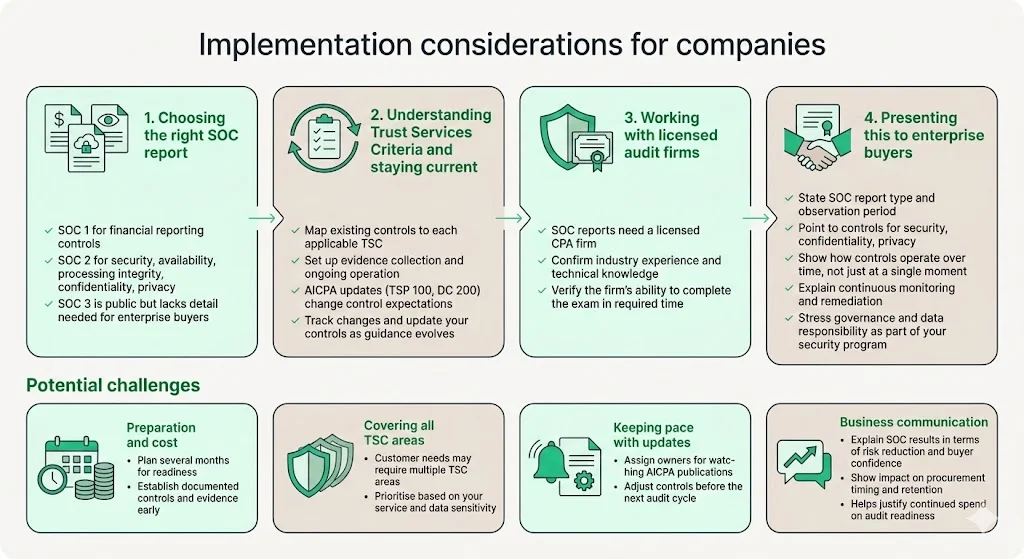

Organizations pursuing SOC attestations must first identify which report type aligns with customer requirements and service offerings. SOC 1 addresses controls relevant to customer financial reporting, typically applicable to payroll processors or transaction processing services. SOC 2 evaluates controls related to Trust Services Criteria—security, availability, processing integrity, confidentiality, and privacy—making it the relevant framework for most technology vendors, SaaS providers, and service organizations handling customer data. SOC 3 provides a general-use summary of SOC 2 findings suitable for public disclosure but lacks the detailed control descriptions enterprise buyers require.

Understanding Trust Services Criteria and mapping existing controls to TSC requirements represents the foundational work for SOC 2 readiness. Organizations must document how controls address each applicable criterion, establish evidence collection processes, and demonstrate that controls operate consistently over time. The AICPA periodically updates its guidance—including significant 2022 updates to TSP Section 100 and DC Section 200—impacting control requirements, points of focus, and reporting standards. Organizations must track these updates and adjust control frameworks accordingly to maintain alignment with current standards.

Working with a licensed CPA firm authorized to perform AICPA attestation engagements is mandatory for SOC reports. Not all accounting firms maintain the expertise or credentials necessary to conduct SOC audits; organizations should verify that selected auditors possess relevant experience with their industry, understand the technical controls being evaluated, and can complete examinations within required timeframes.

How to position this for enterprise clients

Vendor procurement materials should prominently reference SOC report status, observation periods, and applicable Trust Services Criteria. Rather than generic statements about "industry-leading security," effective positioning specifies: "We maintain controls aligned with AICPA's Trust Services Criteria for security, confidentiality, and privacy, validated through our SOC 2 Type II examination covering a 12-month observation period."

Organizations should articulate how they address each Trust Services Criterion relevant to customer concerns. Enterprise buyers evaluating confidentiality controls want specifics: encryption standards, data classification procedures, access restrictions, and monitoring mechanisms. Referencing AICPA frameworks provides a common language for these discussions, enabling vendors to demonstrate alignment with recognized standards rather than explaining proprietary security approaches.

Demonstrating ongoing monitoring, remediation tracking, and governance mechanisms tied to AICPA standards addresses enterprise questions about sustained compliance. SOC 2 Type II reports document control effectiveness over time, but enterprise buyers increasingly ask about continuous monitoring between annual audits, how organizations address identified exceptions, and what governance structures ensure controls remain effective as systems evolve.

The governance and ethics dimensions inherent in AICPA's professional standards support broader narratives around data stewardship and organizational accountability. Enterprise buyers evaluate vendor stability, operational maturity, and risk management practices alongside technical controls; positioning SOC 2 compliance within a comprehensive security program demonstrates that data protection represents an operational discipline rather than a compliance checkbox.

Potential challenges and how to address them

SOC audits require significant investment in preparation, evidence collection, and audit fees. Organizations should plan 4-6 months for initial SOC 2 readiness, establishing documented controls, implementing evidence collection processes, and conducting pre-audit assessments before engaging auditors. This timeline extends if gaps exist in existing control frameworks or if organizations lack documented policies and procedures required for attestation.

Mapping controls to all five Trust Services Criteria categories—particularly when enterprise customers require all criteria rather than security alone—introduces complexity. Organizations should prioritize based on customer requirements and service characteristics. SaaS providers handling sensitive customer data typically must address security, confidentiality, and privacy criteria; availability becomes critical for services where downtime impacts customer operations; processing integrity applies to services performing data transformations or calculations affecting customer outcomes.

Maintaining current knowledge of AICPA guidance updates requires periodic review and alignment of internal practices with evolving standards. Organizations should designate ownership for monitoring AICPA publications, assessing impact on existing controls, and implementing necessary adjustments before audit cycles. This proactive approach prevents audit findings related to outdated control implementations that no longer align with current criteria.

Communicating the value of SOC attestations to non-finance stakeholders—particularly procurement, legal, and executive leadership—requires translating audit outcomes into business benefits. Security and compliance teams should position SOC 2 completion in terms of risk reduction, customer trust, market access, and competitive positioning rather than technical control validation. Quantifying the procurement acceleration and customer retention benefits of maintaining current attestations helps justify ongoing investment in audit readiness.

Real-world examples and use cases

SaaS vendors entering enterprise markets consistently encounter SOC 2 requirements during initial customer conversations. A typical scenario: a mid-market SaaS company pursues its first Fortune 500 customer, only to discover that procurement requires a current SOC 2 Type II report before contract execution. The vendor invests 5 months establishing controls, collecting evidence, and completing the initial audit, then uses that attestation to accelerate subsequent enterprise deals. The SOC 2 report becomes a reusable asset addressing security questions across multiple procurement cycles.

Organizations experiencing data breaches or security incidents face intensified customer scrutiny around security controls. Following an incident, customers demand evidence of remediation and control improvements. Obtaining a SOC 2 Type II report provides independent validation that security controls have been enhanced and operate effectively, helping restore customer confidence through third-party attestation rather than vendor assurances alone.

Vendors leveraging the AICPA SOC for Cybersecurity framework differentiate by providing enterprise customers with comprehensive cybersecurity program reporting beyond traditional SOC 2 scope. This positions the vendor as demonstrating enterprise-grade security maturity, board-level governance, and risk management sophistication that exceeds baseline compliance requirements. For organizations selling to highly regulated industries or government entities, this additional attestation addresses elevated security expectations.

Enterprise-grade security and controls aligned with AICPA frameworks serve as differentiators during competitive vendor selections where multiple providers offer similar functionality. Procurement teams evaluating feature parity among competing solutions elevate security attestations and compliance posture as decision criteria. Organizations with current SOC 2 Type II reports, documented control frameworks, and transparent reporting gain preference over competitors requiring extended security reviews or presenting unverified security claims.

The future of AICPA and data protection standards

The data risk landscape continues evolving with cloud computing architectures, artificial intelligence implementations, and distributed workforces creating new security and privacy challenges. The AICPA adapts frameworks through guidance updates, new points of focus, and emerging practice areas addressing contemporary risks. Recent updates to TSP Section 100 and DC Section 200 reflect evolving expectations for control rigor, evidence documentation, and reporting transparency.

Enterprise buyers will intensify demands for data protection transparency, vendor accountability, and audit assurance as regulatory requirements expand and data breach consequences escalate. Organizations should anticipate more granular scrutiny of subprocessors, supply chain security, data residency controls, and incident response capabilities. The role of independent attestation in vendor risk management will grow as internal security assessments prove insufficient for complex, interconnected service ecosystems.

The accounting profession's involvement in cybersecurity and data protection continues expanding beyond traditional financial controls. CPAs increasingly provide cybersecurity consulting, privacy program assessments, and risk management advisory services. This evolution reflects enterprise recognition that security assurance requires independent expertise, standardized evaluation criteria, and professional accountability—precisely what AICPA frameworks provide.

Companies selling to enterprise clients should position ahead of these trends by establishing mature control frameworks, maintaining continuous audit readiness, and proactively communicating security posture through AICPA-aligned attestations. Organizations treating SOC 2 as an annual compliance exercise rather than an operational discipline will struggle as expectations intensify. Sustained competitive advantage comes from embedding security and data protection as core operational capabilities that produce compliance outcomes naturally rather than through last-minute audit preparations.

Conclusion

The AICPA functions as the standards-setting body whose frameworks enable organizations to demonstrate data protection capabilities through independent attestation. For companies targeting enterprise customers, AICPA-developed standards—particularly SOC 2 and the Trust Services Criteria—provide the common language and evaluation framework that procurement teams require before executing vendor contracts.

AICPA frameworks support data protection through explicit confidentiality and privacy criteria, security baseline requirements, and attestation processes conducted by licensed CPA firms following standardized examination procedures. These frameworks translate abstract security claims into documented evidence validated by independent auditors, creating the assurance enterprise buyers demand.

For organizations selling to enterprise clients, alignment with AICPA standards represents strategic positioning in vendor evaluations and risk assessments. Demonstrating controls that meet Trust Services Criteria, maintaining current SOC 2 Type II attestations, and communicating security posture through AICPA frameworks accelerates procurement cycles and enables market access that self-assessed security documentation cannot replicate.

FAQs

1) What is the AICPA and what does it do?

The AICPA is the national professional organization of Certified Public Accountants in the United States with more than 428,000 members, founded in 1887, that sets ethical standards and U.S. auditing standards. The organization develops the Uniform CPA Examination, establishes auditing and attestation standards including the SOC framework, and maintains professional conduct requirements for CPAs. The AICPA creates the frameworks and criteria that licensed CPA firms use when conducting audits and attestations for service organizations.

2) What is the difference between CPA and AICPA?

CPA refers to Certified Public Accountant—an individual credential requiring specific education, work experience, and successful completion of the Uniform CPA Examination. The AICPA is the professional organization representing CPAs, setting the standards CPAs must follow, developing the examination CPAs must pass, and establishing the ethical code CPAs must uphold. Individual accountants become CPAs by meeting state licensing requirements; those CPAs may choose to join the AICPA as members, though CPA licensure itself is granted by state boards of accountancy, not the AICPA.

3) Is AICPA the same as CIMA?

The AICPA and CIMA (Chartered Institute of Management Accountants) are distinct organizations that formed a joint venture in 2012. The Association of International Certified Professional Accountants is the global voice of the accounting and finance profession, founded by the American Institute of CPAs and The Chartered Institute of Management Accountants. The AICPA focuses on U.S. CPA standards, auditing, and attestation, while CIMA specializes in management accounting. The joint venture created the CGMA (Chartered Global Management Accountant) designation but the organizations maintain separate memberships, credentials, and standard-setting functions.

4) Who does AICPA apply to?

AICPA standards apply to licensed CPAs conducting audits, attestations, and professional services in the United States. Organizations seeking SOC reports or other AICPA-framework attestations must engage licensed CPA firms authorized to perform these examinations. Service organizations across industries—particularly technology vendors, SaaS providers, data processors, and any company handling customer data or providing services affecting customer operations—use AICPA frameworks to demonstrate security and data protection controls to enterprise clients. While the AICPA is a U.S. organization, its SOC frameworks have become internationally recognized standards referenced in vendor contracts worldwide.